by Conrad Meertins | Dec 9, 2024 | Uncategorized

Whether you’re selling your home or refinancing your mortgage, an appraisal is a critical step in the process. Appraisers evaluate your property to determine its market value. However, certain issues, or “appraisal red flags,” can lower your home’s value. Let’s explore these red flags and how you can avoid them.

Introduction

Picture this: You’re ready to make a big move. You’ve got a buyer lined up for your home or you’re all set to refinance your mortgage. But there’s one crucial step left – the home appraisal. Enter the appraiser, the person who gets to decide the market value of your home. This individual walks through your property, eyes sharp, jotting down notes, assessing every nook and cranny.

Now, let’s talk about something called “appraisal red flags.” Think of these as the little gremlins that could potentially lower your home’s value in the eyes of the appraiser. It could be something as significant as a crack in the foundation or as subtle as outdated electrical systems.

This article will guide you through these red flags, helping you understand what they are and why it’s so important to be aware of them. Because, let’s face it, no one wants a lower appraisal than expected, right? So, let’s dive in and demystify these appraisal red flags.

Understanding Appraisal Red Flags

You’ve done everything you can think of to get your home ready to sell. Fresh paint on the walls, new fixtures in the bathroom, even a few strategic landscaping improvements to enhance curb appeal.

But when the appraiser arrives, they point out several issues that you hadn’t even considered. Suddenly, your home’s market value takes a hit. This is the power of “appraisal red flags.”

So, what exactly are these red flags? In the simplest terms, appraisal red flags are issues or conditions that can negatively impact the value of your home in the eyes of an appraiser. These can range from obvious physical problems, like a cracked foundation or outdated systems, to more subtle issues, like unpermitted renovations or even factors outside your home, like the gas station next door..

Now, you might be wondering: why should I care about these red flags? Well, in the world of real estate, knowledge is power. Being aware of potential appraisal red flags can help you anticipate issues before they become a problem, allowing you to address them proactively. Whether you’re a homeowner preparing for an appraisal or a buyer trying to understand the value of a potential investment, understanding these red flags can be a game-changer.

Think of it this way: each red flag is a conversation between you and the appraiser. They’re saying, “Hey, this could be a problem,” and you have the opportunity to respond, either by fixing the issue or by adjusting your expectations about your home’s value. So, let’s dive into these conversations and learn how to navigate them effectively.

Top 5 Appraisal Red Flags

Let’s dive into the nitty-gritty, shall we? Here are the top five red flags appraisers are on the lookout for when they swing by your property.

First up, Structural Issues. Think of your home as a human body, the structure is the skeleton that holds everything together. If there are cracks in the foundation or the roof looks like it’s seen better days, it’s like a broken bone or a bad back. It’s a serious problem. These types of issues can significantly knock down your home’s value because they’re costly to repair and can lead to other problems down the line. The key here is that if its observable to the appraiser that it’s something that he will likely notate in his or her report.

Next, we have Outdated Systems. If your home’s electrical, plumbing, or HVAC systems are older than the cast of Friends, you’ve got a problem. Appraisers know that outdated systems can be a ticking time bomb of expensive repairs. Plus, they’re not as efficient or safe as their modern counterparts. The appraiser is not a home inspector, but its easy to see corrosion on pipes, exposed electrical wires or leaking water heaters.

Thirdly, Poor Maintenance. You know that peeling paint you’ve been meaning to address or that leaky roof you’ve been ignoring? Yeah, appraisers notice that too. Signs of neglect like these are red flags because they suggest there might be other, potentially more serious issues lurking beneath the surface.

The fourth red flag is Unpermitted Additions. That DIY sunroom might seem like a selling point to you, but if it was done without the proper permits, it could be a liability. Unpermitted additions can lead to serious legal and safety issues, and appraisers may mention them in his report.

Finally, Neighborhood Factors. You might have the nicest house on the block, but if your block happens to be right next to a noisy highway, it’s going to hurt your appraisal. Appraisers take into account the market’s reaction to such influences when determining a home’s value.

In essence, appraisers are like home detectives, looking for clues that tell the true story of a property’s value. These five red flags are key indicators they use in their investigation. So, if you’re preparing for an appraisal, it’s wise to address these issues head-on. Don’t try to hide them or hope they’ll go unnoticed. Trust me, they won’t.

Tips to Avoid Appraisal Red Flags

So, you’ve got a good handle on what appraisers are on the lookout for – those pesky red flags that could potentially lower your home’s value. But what can you do about it? How can you make sure your home passes the appraisal with flying colors? Don’t worry, I’ve got your back. Let’s roll up our sleeves and dive into some practical tips that can help you sidestep these common appraisal pitfalls.

Firstly, take a good, hard look at your home. And I mean really look. Put yourself in the shoes of an appraiser. Are there any glaring issues that jump out at you? Cracked walls? Peeling paint? Outdated electrical systems? These are all things you’ll want to address before the appraiser’s visit.

Next, get your hands on a home inspection checklist. This can be a real lifesaver. It’ll guide you through each part of your home, helping you identify and fix potential red flags. And trust me, it’s a lot easier to fix these issues before the appraiser points them out.

Now, let’s talk about those unpermitted additions. You know, that fancy new deck you built last summer? If you didn’t get the proper permits for it, it could be a real thorn in your side during the appraisal. So, make sure you’ve got all your paperwork in order. If you’re missing any permits, now’s the time to get them.

Finally, remember that factors outside your home can also impact your appraisal. You might not be able to control the noise from the nearby highway, but you can make your home more appealing in other ways. A well-maintained garden, a new coat of paint, or even some attractive outdoor lighting can all help to boost your home’s curb appeal.

As Tom Horn, a seasoned appraiser from the Birmingham Appraisal Blog, wisely points out, “The best defense is a good offense.” By taking a proactive approach and addressing potential red flags before the appraisal, you’ll be in a much stronger position. So, don’t wait for the appraiser to knock on your door. Get ahead of the game and make sure your home is in tip-top shape.

Conclusion

So, there you have it, folks. We’ve taken a journey down the less-traveled road of home appraisal, shedding light on the elusive ‘red flags’ that can potentially play spoilsport in your home’s valuation game. Structural issues, outdated systems, poor maintenance, unpermitted additions, and neighborhood factors – they all play a pivotal role in determining the value of your home in the eyes of an appraiser.

Now, you might be thinking, “This all sounds pretty daunting, doesn’t it?” But here’s the kicker – it doesn’t have to be. As a homeowner, you hold the power to ensure a successful appraisal. It’s all about staying proactive, keeping your home in good shape, and addressing potential issues before they escalate into full-blown red flags. Remember, a well-maintained home is not just a pleasure to live in; it’s also a goldmine when it comes to appraisal.

So, go ahead. Take a good look around your home. Is there a crack in the foundation you’ve been ignoring? An outdated electrical system that’s due for an upgrade? Or maybe an unpermitted addition that needs to be legitimized? Tackle these issues head-on, and you’ll be well on your way to acing that appraisal.

In the end, it’s not just about getting a good appraisal. It’s about maintaining your home to the best of your ability, and ensuring it reflects the true value it holds. Because, let’s face it, your home is more than just a property – it’s a reflection of you. And you, my friend, are priceless.

by Conrad Meertins | Dec 2, 2024 | Uncategorized

Getting your property appraised can be a daunting task, especially if you’re unsure about how to prepare for it. But fear not! This guide is here to help you get your home ready for the most accurate valuation possible.

Introduction

So, you’re about to dive into the world of home appraisals. It might feel like uncharted territory, like setting foot on the moon without an astronaut’s guide. But here’s the thing: you’re not alone in this journey. I’m here to navigate you through the twists and turns, the ups and downs, and the ins and outs of home appraisals. But first, let’s get our bearings.

A home appraisal, in its simplest form, is a professional evaluation of your property’s worth. It’s like a health check-up, but for your house. And just like your health, it’s crucial to get an accurate diagnosis. An incorrect appraisal could mean selling your home for less than it’s worth or, conversely, pricing it so high that it languishes on the market.

Now, I know what you’re thinking: “Great, another thing to stress about!” But hold your horses, because this guide is here to ease your worries and help you prepare for an accurate home appraisal. Think of it as your personal playbook, filled with insider tips, practical steps, and sage advice. So, strap in, and let’s get started on this journey to a successful home appraisal.

Understanding the Home Appraisal Process

Imagine you’re a detective. Your mission? To discover the true value of a property. That’s what the home appraisal process is all about. It’s an investigation of sorts, an exploration into the value of your property. Sounds thrilling, right? Let’s dive in.

First off, it’s important to understand that a home appraisal isn’t a one-size-fits-all process. It’s a personalized investigation, tailored to your property. It’s about assessing the unique features and characteristics of your home, from the age and condition of the property to its location and size.

Think about it. Would a vintage, Victorian-style home in a historic district be valued the same as a modern, minimalist apartment in the city center? Probably not. And that’s where the appraisal process comes in. It’s about understanding what makes your property unique and how these factors contribute to its value.

So, how does it work? Well, it starts with a professional appraiser visiting your property. They’ll inspect the home, taking note of its condition, size, design, and any unique features. They’ll also consider the property’s location and how it compares to similar properties in the neighborhood.

But it doesn’t stop there. The appraiser will also take into account market trends and recent sales data of comparable homes in your area. It’s a thorough process, combining both the physical attributes of your home and the larger real estate market context.

So, what’s the takeaway here? A home appraisal is a holistic process, one that considers a wide range of factors to determine the true value of your property. It’s not just about what your home looks like, but also where it’s located, how it compares to similar properties, and how it fits into the broader real estate market.

In the end, understanding the home appraisal process is like having a roadmap. It helps you navigate the journey, giving you a clearer idea of what to expect and how to prepare. So, ready to embark on this appraisal adventure? Let’s move on to some top tips to help you prepare.

Top Home Appraisal Tips

Picture this: you’re about to invite a professional appraiser into your home, and you’re hoping for the highest valuation possible. What can you do to tip the scales in your favor? Here are some insider tips to help you prepare for a home appraisal that reflects the true value of your property.

- Understand the Market: The value of your home is largely determined by the current real estate market conditions in your area. So, do your homework. Look at the recent sales prices of similar homes in your neighborhood. Having a sense of the market can help you set realistic expectations for your own home’s value.

- Highlight the Positives: Every home has its unique features. Maybe it’s a recently renovated kitchen, a large backyard, or a convenient location. Make sure these highlights are not overlooked. Point them out to the appraiser and explain why they add value to your home.

- Don’t Forget About the Small Improvements: While major renovations certainly increase a home’s value, don’t underestimate the power of small improvements. A fresh coat of paint, new hardware on cabinets, or updated lighting fixtures can make a big difference in the overall appeal of your home.

- Keep Up with Regular Maintenance: A well-maintained home is a valuable home. Regular maintenance tasks like cleaning gutters, servicing HVAC systems, and repairing leaky faucets show that you take good care of your property. This can positively influence an appraiser’s assessment of your home’s condition.

- Be Present During the Appraisal: It’s important to be home during the appraisal. You can answer any questions the appraiser might have and provide additional information about your home’s features and improvements. Plus, it gives you a chance to showcase your home in the best light.

Remember, an appraisal isn’t just about tallying up square footage and counting bathrooms. It’s about assessing the overall quality, condition, and appeal of a home. By understanding the process and taking these steps, you can help ensure your home is appraised at its true worth.

Practical Steps to Prepare for Home Appraisal

Before we dive into the meat of this section, let’s take a moment to imagine a scenario. Picture this: You’re about to host a dinner party for some very important guests. You’d naturally want your home to look its best, right? You’d clean, declutter, and maybe even do some minor repairs. Preparing for a home appraisal isn’t much different.

First things first, clean and declutter. Just like your dinner guests, appraisers are people too. And let’s be honest, no one likes to navigate through a maze of mess. A clean, organized home can make a positive impression.

Next, repair and maintain. Remember that leaky faucet you’ve been meaning to fix? Now’s the time. Appraisers look for signs of neglect or damage that could affect the home’s value. Addressing these issues beforehand can save you from potential valuation dings. It’s not just about major repairs either. As mentioned earlier, regular maintenance like servicing your HVAC system or cleaning your gutters can also make a difference.

Finally, document improvements. Have you renovated the kitchen or installed a new roof? Keep a record of these improvements. Appraisers aren’t just looking at your home’s current condition, they’re also interested in its history. Providing documentation of renovations and upgrades can help justify a higher valuation.

These practical steps aren’t just about impressing the appraiser. They’re about presenting your home in the best light possible. It’s about showing respect for your property and its value. So, don’t think of it as a chore. Consider it an opportunity to showcase your home’s true potential.

Common Mistakes to Avoid During Home Appraisal

When it comes to the home appraisal process, even the most well-intentioned homeowners can unwittingly sabotage their own efforts. Here are some common missteps you’ll want to sidestep for a smooth and successful appraisal:

- Ignoring Minor Repairs: I know I might sound like a broken record here, but small issues like leaky faucets, cracked windows, or chipped paint may seem inconsequential, if multiplied by 10, can suggest to an appraiser that the home hasn’t been well-maintained. Make these repairs before the appraiser visits to ensure your home is seen in the best light.

- Overestimating the Value of Renovations: Not all home improvements are created equal. While you may value your custom-made wine cellar, an appraiser might not see it as a significant value-add. Be realistic about the financial return of your renovations.

- Failing to Document Improvements: If you’ve made significant upgrades to your home, like a new roof or HVAC system, make sure you have the documentation to prove it. Without this, the appraiser might overlook these improvements.

- Being Absent During the Appraisal: While you don’t need to hover, being present allows you to answer any questions the appraiser might have. Plus, it gives you a chance to highlight the features you love about your home.

Avoiding these common mistakes can go a long way towards ensuring your home is appraised accurately. Remember, preparation is key. By understanding the appraisal process and taking the time to properly prepare, you’ll be setting your home – and yourself – up for success.

Utilizing Resources for a Successful Home Appraisal

So, you’ve done the hard yards. You’ve decluttered, fixed the wonky step, and even spruced up the garden. But, are you really ready for that home appraisal? There’s one more step that can help you ensure you’re not leaving any stone unturned – utilizing resources.

Imagine you’re about to bake a cake for the first time. You have all the ingredients, but do you just toss them into a bowl and hope for the best? Probably not. You’d likely follow a recipe, right? Think of resources like your recipe for a successful home appraisal.

One such resource is a home appraisal preparation checklist. Comprehensive checklists can guide you through the preparation process. They help you track your progress, ensure you’re covering all bases, and give you a sense of confidence that you’re on the right path. If you’d like to grab mine, visit the link below. I know what appraisers look for and what homeowners often overlook. By using these resources, you’re essentially getting insider tips on how to make your home shine in the eyes of an appraiser.

And it’s not just about getting a higher valuation. An accurate appraisal can save you from overpricing or underpricing your property, both of which can lead to financial losses or missed opportunities.

So, don’t just wing it. Use the resources available to you. They’re like your secret weapon for a successful, accurate home appraisal. After all, when it comes to something as important as your home’s value, wouldn’t you want to be as prepared as possible?

Conclusion

As I wrap up our guide, let’s revisit the key steps to ensure your property is well-prepared for an accurate home appraisal. It’s more than just a casual stroll through your property. It’s about presenting your home in its best light, making sure it’s clean, decluttered, and well-maintained. It’s about keeping a detailed record of all improvements and renovations.

Remember, it’s not about tricking the appraiser with superficial enhancements, but genuinely showcasing the value your property holds. Like a proud parent at a school open day, you want to highlight your home’s best features, but not hide its quirks. Every home has them, and they’re part of what makes your property unique.

Taking the time to prepare your property properly is not just about getting a higher appraisal value. It’s about understanding the true value of your home and being able to present it confidently. It’s about being an informed homeowner who knows their property inside out.

The benefits of an accurate property valuation extend beyond the appraisal day. It helps in setting a fair selling price, securing a mortgage, or even for insurance purposes. It’s a critical step in your homeownership journey, and we hope this guide has made the process a little less daunting.

Don’t forget to utilize resources like the home appraisal preparation checklist from our website. These tools are designed to guide you through the process and ensure nothing slips through the cracks.

In the end, the goal is to make the home appraisal process as smooth and successful as possible. And remember, preparation is the key to success. So take a deep breath, roll up your sleeves, and let’s get your property ready for its big day. You’ve got this!

by Conrad Meertins | Nov 6, 2024 | Uncategorized

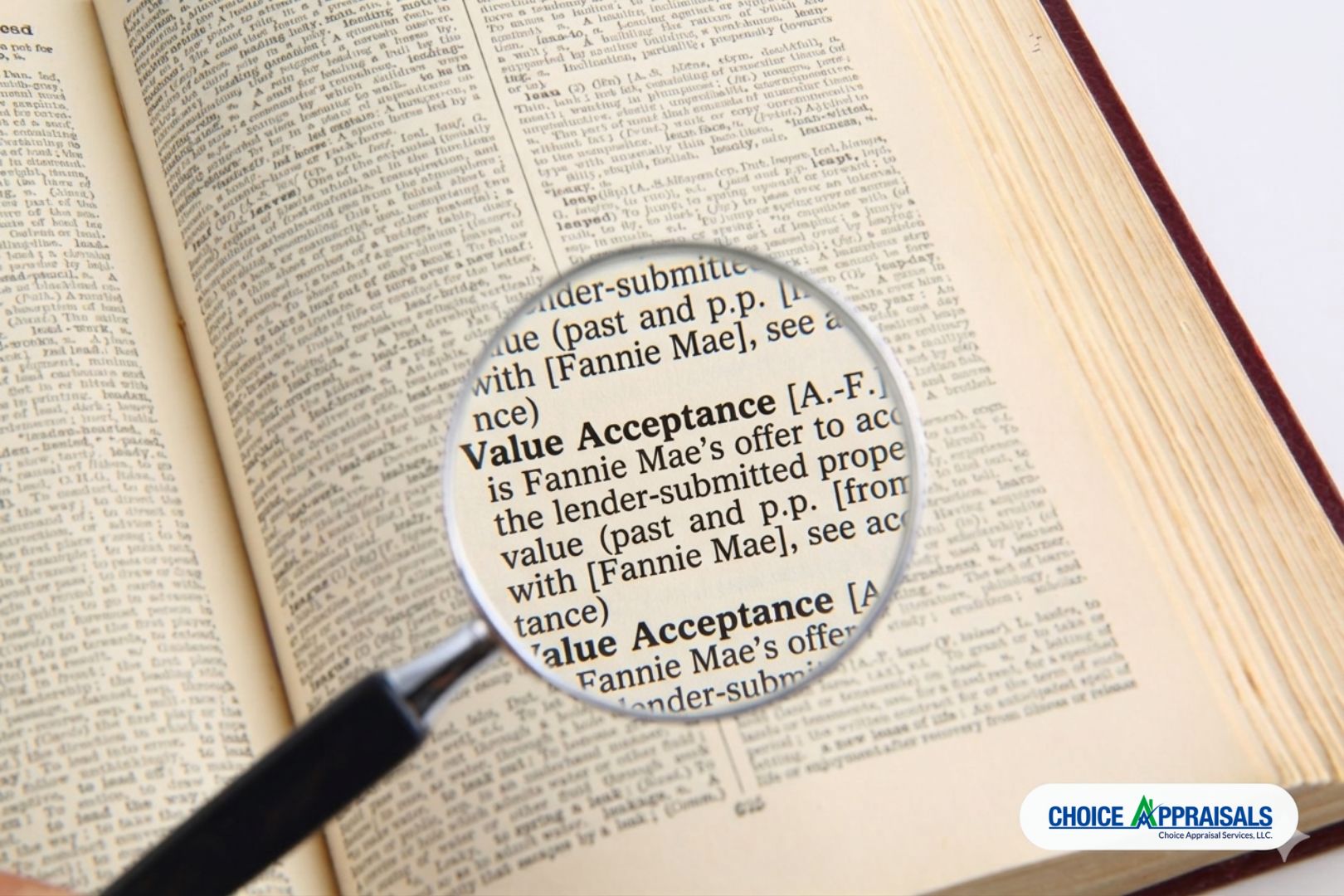

If you have been told your loan might not require a traditional appraisal, you have run into what used to be called an appraisal waiver. As of September 3, 2025, Fannie Mae retired that term and now uses value acceptance instead. The name changed, and the programs around it have expanded, so it is worth understanding what these options actually are. As an appraiser, my goal here is not to tell you what to do or what your home is worth. It is to explain the landscape clearly so you can recognize which path your transaction is on and ask good questions.

Let me walk through it the way I would explain it to someone sitting across my desk.

What changed, and what the terms mean now

For years, lenders could sometimes accept a property’s value without ordering a full appraisal, and that was commonly called an “appraisal waiver.” In September 2025, Fannie Mae replaced that phrase with value acceptance, because the older term implied an appraisal was the default that was being skipped. The new language describes the process more accurately: the lender submits a value, and the program accepts it when the data and modeling support doing so for an eligible loan. If you still see “appraisal waiver” in older articles or conversations, people are almost always describing what is now called value acceptance.

The programs have also grown. In the first quarter of 2025, the eligible loan-to-value ratio for value acceptance on primary residence and second-home purchases increased from 80 percent to 90 percent, which means more transactions can now qualify.

One thing to keep in mind before we go further: these are Fannie Mae and Freddie Mac programs. Government loans, such as FHA and VA, follow their own appraisal rules, so if you are using one of those, value acceptance may not apply to your transaction.

The options, in plain terms

Think of these as a spectrum, running from no property visit at all to a full traditional appraisal.

- Value acceptance. For eligible transactions, the lender-submitted value is accepted with no appraisal required. This relies on data and modeling rather than a visit to the property.

- Value acceptance + property data. There is no traditional appraisal, but a trained third-party data collector visits the property to document the interior and exterior. That information is submitted in a standardized format. The collector gathers facts; they do not develop an opinion of value.

- Automated Collateral Evaluation (ACE) and ACE + Property Data Report (PDR). These are Freddie Mac’s comparable programs. ACE uses data and models, and ACE + PDR adds an on-site property data collection step.

- Desktop, hybrid, and traditional appraisals. When an appraisal is part of the loan, it can be a traditional appraisal (an appraiser inspects the property in the usual way), a desktop appraisal (completed from property data and records), or a hybrid appraisal (the property visit and the appraiser’s analysis are handled separately). In each case, the appraiser develops an independent, impartial opinion of value.

How the path is decided

Here is a point that surprises a lot of buyers: you do not choose your path, and neither does your agent. Eligibility is determined through the lender’s automated underwriting on a loan-by-loan basis, using the data available for the property and the specifics of your loan. Factors like your loan-to-value ratio and how much comparable data exists for the property influence which options are offered.

That is simply how the system works. It is helpful to know so you are not caught off guard when a lender tells you no appraiser will be visiting, or when a data collector schedules a visit even though no traditional appraisal is being performed.

What each method does and does not do

It helps to understand the trade-offs factually, without treating any option as good or bad.

Value acceptance and the automated programs are built for speed and lower upfront cost. They lean on data and modeling. By design, they do not include an appraiser physically walking the property and forming an independent opinion of value.

A traditional appraisal does include that independent, in-person analysis. An appraiser observes the property, researches the local market, and develops a supportable conclusion. It generally takes more time and carries a fee.

Neither is universally “better.” They answer the lender’s need in different ways, and the right fit depends on the transaction, which is why the program eligibility is decided case by case rather than by preference.

What a homebuyer can reasonably do

The most useful posture is to understand your situation rather than try to steer the outcome. A few practical steps:

- Ask your lender which path applies. They can tell you whether your loan is using value acceptance, value acceptance + property data, or a full appraisal, and what that means for your timeline.

- Understand the basis for the value. If you are moving forward without a traditional appraisal, it is reasonable to ask how the value was determined and what supports it. You are entitled to understand the figure your loan relies on.

- Keep accurate records. If you own the property and have completed improvements, having documentation of what was done and when, including permits where applicable, gives an appraiser or data collector accurate, factual information to work from.

- Know your options. If you have questions about the valuation method on your loan, you can ask your lender what the choices are, including whether a traditional appraisal is part of them.

Notice that none of this is about influencing a number. The value, when an appraisal is involved, is the appraiser’s independent and impartial conclusion. Your role is to understand the process, not to push it in a direction.

A final thought

Value acceptance and its related programs are part of a broader shift toward using data and technology to confirm a property’s value, paired with clearer language to describe it. For a homebuyer, the practical takeaway is straightforward. Learn which valuation path your loan is on, ask your lender how the value was reached, and recognize that an appraisal, when it is part of the deal, provides an independent and impartial opinion rather than a number anyone can steer.

The more you understand how these pieces fit together, the more confident you can be in your decisions. And as with most things in real estate, the guidelines keep evolving, so it is always worth asking what is current.

by Conrad Meertins | Sep 30, 2024 | Uncategorized

Are you considering buying or selling a home in Louisville’s MLS Area 6, which includes Buechel, Highview, Okolona, and Fern Creek? Understanding current market trends is crucial for making informed decisions. Let’s dive into how these neighborhoods are faring in today’s real estate landscape.

Current Market Snapshot (as of September 28, 2024)

- Active Listings: 242

- Median Listing Price: $315,900

- Average Days on Market: 56 days

- Median Days on Market: 34 days

These numbers tell an interesting story. With homes staying on the market for nearly two months, buyers may find more room for negotiation, especially on properties listed for 50+ days. Sellers should note that pricing strategy is key in this market.

Price Trends: A Tale of Two Markets

- Median Listing Price (Active): $315,900

- Median Sales Price (Sold): $250,000

- Average Days on Market (Sold): 28 days

- Median Days on Market (Sold): 7 days

The significant gap between listing and selling prices suggests that while sellers are optimistic, buyers are more cautious. However, homes priced right are still moving quickly, often in less than a two weeks.

Supply & Demand: A Clearer Picture

- Current Active Listings: 242 (as of September 28, 2024)

- Total Sold Properties: 2,402 (from January 1, 2023 to September 28, 2024)

Let’s break this down:

- The 242 active listings represent what’s available right now in Buechel, Highview, Okolona, and Fern Creek.

- 2,402 properties sold over the past 21 months, averaging about 114 sales per month.

This suggests strong ongoing demand in Area 6, with current inventory limited compared to the consistent sales rate. It’s a market that favors sellers, but buyers who act decisively on well-priced homes can still find opportunities.

Property Characteristics

| |

Active Listings

|

Sold Properites

|

| Average Size |

1722 sq ft |

1525 sq ft |

Homes currently on the market tend to be larger and relatively newer. This could explain the higher listing prices and longer selling times, as these properties may be at the upper end of the local market.

What This Means for You

For Buyers:

- Be prepared for competition, especially for well-priced homes.

- Don’t hesitate to negotiate, particularly on homes that have been listed for a while.

- Consider the long-term value of larger, newer homes currently available.

For Sellers:

- Pricing is critical. Homes priced right are still selling quickly.

- Be prepared for negotiations, especially if your home has been listed for over 50 days.

- Highlight features that make your property stand out, such as size or recent updates.

Neighborhood Spotlight

Buechel, Highview, Okolona, and Fern Creek each offer unique attractions:

- Buechel: Known for its diverse community and proximity to Bardstown Road.

- Highview: Offers a suburban feel with easy access to downtown Louisville.

- Okolona: Popular for its parks and family-friendly atmosphere.

- Fern Creek: Balances rural charm with modern conveniences.

These varied neighborhoods contribute to the diverse housing options in Area 6, catering to a wide range of preferences and budgets.

Looking Ahead

The real estate market in MLS Area 6 reflects a balance between opportunity and challenge. While inventory is limited compared to recent sales volume, the longer days on market for current listings suggest a shift towards a more balanced market.

For both buyers and sellers, understanding these local trends is key to making informed decisions. Whether you’re looking to buy your first home, upgrade to a larger property, or sell your current house, the diverse neighborhoods of Area 6 offer something for everyone.

Interested in a more personalized analysis of your specific situation in Buechel, Highview, Okolona, or Fern Creek? Don’t hesitate to reach out. We’re here to help you navigate this dynamic market with confidence.

by Conrad Meertins | Jun 24, 2024 | Uncategorized

Ever wondered how appraising a charming Victorian mansion differs from a modern suburban home? Historical properties offer unique challenges and opportunities in the appraisal process.

The allure of these properties lies in their rich history and architectural beauty, making them more than just real estate—they’re pieces of history.

This article delves into the intricacies of appraising historical properties, highlighting the unique factors that affect their value.

From understanding their historical significance to navigating regulatory hurdles, we’ll guide you through the essential aspects of this specialized field.

By mastering the art of appraising historical properties, you’ll be better equipped to preserve their legacy while ensuring accurate valuations. Join me as we uncover the fascinating world of historical property appraisals and equip yourself with the knowledge to navigate this rewarding yet challenging domain.

Understanding Historical Properties

Understanding historical properties begins with recognizing what qualifies them as historical. These properties, often at least 100 years old, possess architectural, cultural, or historical significance.

For instance, a Victorian mansion built in the 19th century may feature intricate woodwork and original stained glass, representing the craftsmanship of its era.

Historical properties are often listed on registers like the National Register of Historic Places, which not only acknowledges their significance but can also provide tax incentives for preservation.

The historical significance can elevate a property’s value, but it also demands careful maintenance and adherence to preservation standards.

Consider the Conrad-Caldwell House in Louisville, KY, an exquisite Richardsonian Romanesque mansion. It stands as a testament to meticulous preservation and historical integrity.

For appraisers, understanding these elements is crucial. It involves assessing not just the physical attributes but also the historical context, making it essential to approach these appraisals with a blend of historical knowledge and technical expertise.

Unique Factors Influencing Appraisal Values

Appraising historical properties involves unique factors that significantly influence their values. Historical significance is a primary factor, as properties associated with notable events or figures can command higher appraisals.

Imagine the birthplace of a famous author or a building pivotal in a historic event—its unique story can greatly increase its value.

Architectural integrity also plays a crucial role. Properties retaining original features like period-specific woodwork, stained glass, or original facades often appraise higher.

Take the Brennan House in Louisville, KY, for example. It’s a prime illustration of preserved Victorian architecture and original furnishings, adding significant value.

Location and context further impact value. Properties situated in well-preserved historical districts or near other landmarks tend to appraise higher. A historic home in Old Louisville, with its prestigious location and historical surroundings, is a perfect example of this.

These unique factors require appraisers to combine historical insight with market analysis to accurately determine the value of historical properties.

Challenges in Appraising Historical Properties

Appraising historical properties presents several challenges. One major hurdle is the lack of comparable properties. Unlike modern homes, historical properties are unique, making it difficult to find similar sales for accurate comparisons.

Imagine trying to find recent sales of an 18th-century Georgian mansion—it’s not easy, and this complicates value estimation.

Condition and restoration needs are also significant challenges. Historical properties often require extensive maintenance and preservation, impacting their appraised value.

The cost of restoring original features, such as hand-carved woodwork or vintage stained glass, can be substantial. Restoring the woodwork in a Victorian home, for example, can cost tens of thousands of dollars.

Regulatory and zoning issues further complicate appraisals. Properties in historical districts may face strict preservation laws limiting alterations. These restrictions can deter potential buyers, affecting market value.

Understanding these challenges is crucial for accurate appraisals, requiring appraisers to blend historical knowledge with practical considerations of maintenance and legal constraints.

Appraisal Methods for Historical Properties

Appraising historical properties necessitates specialized methods to capture their unique value. The Sales Comparison Approach involves comparing the historical property to similar ones that have recently sold, but finding adequate comparables can be challenging.

Adjustments must be made for unique historical features. For example, a Civil War-era house in Louisville might be compared with other historic homes in the area, factoring in its age, condition, and historical significance.

The Cost Approach estimates the value based on the cost to replicate the property, accounting for depreciation. This method is beneficial for properties with significant restorations.

Estimating the cost to restore a Victorian mansion in Old Louisville to its original state helps determine its value by considering both the replacement cost and depreciation.

The Income Capitalization Approach is useful for historical properties generating income, like converted bed-and-breakfasts (if zoning permits). This method assesses the property’s value based on its income potential, factoring in operating expenses and expected returns.

Understanding these appraisal methods allows for accurate valuations, ensuring historical properties are appraised with their unique characteristics in mind.

Best Practices for Realtors Working with Historical Properties

Realtors working with historical properties should follow best practices to ensure accurate appraisals and successful transactions. First, gathering comprehensive documentation is essential. This includes historical records, previous appraisals, and architectural plans. Collaborating with local historical societies can provide invaluable insights and data.

Preparing the property for appraisal involves highlighting its unique features. Ensure that original elements like period-specific woodwork or stained glass are showcased. Addressing necessary repairs while preserving historical integrity can positively impact the appraisal.

Effective communication with appraisers is crucial. Providing detailed information about the property’s historical significance and any relevant restorations can aid the appraiser’s understanding.

For example, detailing the preservation efforts of a restored Victorian home in Old Louisville helps convey its value.

Networking with preservationists and historical experts can also provide support and additional resources. By following these best practices, realtors can better navigate the complexities of historical property transactions, ensuring accurate appraisals and client satisfaction.

Conclusion

In summary, appraising historical properties requires a nuanced approach that blends historical insight with technical appraisal methods. Key factors influencing value include historical significance, architectural integrity, and location context.

These unique aspects, coupled with challenges like limited comparables, restoration needs, and regulatory constraints, make appraisals complex. Employing methods such as the Sales Comparison, Cost, and Income Capitalization approaches ensures accurate valuations.

For realtors, best practices include gathering thorough documentation, highlighting unique features, effective communication with appraisers, and collaboration with historical experts.

By mastering these practices, realtors can provide precise valuations and expert guidance, navigating the complexities of historical property appraisals.

This not only preserves the legacy of historical properties but also enhances professional credibility and client trust. Understanding and applying these principles is essential for success in appraising and selling historical properties.

by Conrad Meertins | Jun 20, 2024 | Uncategorized

Have you ever wondered how your privacy is protected during a real estate appraisal? Confidentiality isn’t just a courtesy—it’s a critical necessity in the real estate industry. Imagine the peace of mind knowing every detail about your property is handled with the utmost care and discretion. Confidentiality ensures that sensitive information remains secure, fostering a trustworthy relationship between appraisers and clients.

This article will explore why confidentiality is paramount, the standards appraisers adhere to, and how safeguarding your personal data protects your interests. Understanding these aspects will help you appreciate the professionalism behind the scenes and the importance of protecting your information for a smooth and secure real estate transaction.

Importance of Confidentiality

Confidentiality is crucial in real estate appraisals for building trust between clients and appraisers. According to the Uniform Standards of Professional Appraisal Practice (USPAP), appraisers are required to maintain confidentiality, reinforcing the importance of privacy in the appraisal process.

People often ask me if the report will be shared with the county assessor, thus causing their taxes to go up, or if it will go to the IRS. The report is prepared for the client and is only shared with those identified by the client as intended users or when required to do so by law.

For example, if an appraiser discloses a client’s financial details or property specifics without permission, it could lead to identity theft or financial fraud. A breach of confidentiality can also damage an appraiser’s reputation and result in legal consequences. Moreover, confidentiality is essential for maintaining market integrity. If confidential information is leaked, it could influence property values and distort the market.

By prioritizing confidentiality, appraisers not only comply with ethical standards but also uphold the integrity and trust necessary for fair and accurate real estate transactions.

Standards and Practices

The Uniform Standards of Professional Appraisal Practice (USPAP) outlines strict guidelines that appraisers must follow to ensure client information remains secure. These guidelines mandate that appraisers keep all information about the property, the client, and the appraisal itself confidential, unless legally obligated to disclose it.

Fortunately, major technology providers like Microsoft and Google incorporate robust security features into their products to help maintain confidentiality. For instance, Microsoft 365 offers built-in security measures, and Gmail uses technology to keep your emails secure. Even WhatsApp now has encrypted communication to protect your messages. In this world of data breaches, it’s reassuring to know that the big players are taking serious measures. However, it is still important to use good judgment and be careful when using these tools.

Appraisers can also use password management tools like LastPass to create and store complex passwords securely. This minimizes the risk of unauthorized access to sensitive information.

By adhering to these standards and using these tools, appraisers demonstrate their commitment to ethical practices and protect the integrity of the real estate market.

Breach of Confidentiality

A breach of confidentiality in real estate appraisals can have significant repercussions. When an appraiser fails to protect sensitive information, it can lead to severe legal, financial, and reputational damage. For example, if an appraiser discloses a client’s financial status or property details without consent, it could result in identity theft or financial fraud. Such breaches can undermine client trust and the appraiser’s professional credibility.

Hypothetically, imagine a case where a leaked appraisal report reveals private details about a high-profile client. This could lead to a lawsuit and substantial financial penalties for the appraiser involved. Beyond legal consequences, such breaches could distort the real estate market. Confidential information, if exposed, could unfairly influence property values and disrupt fair market assessments.

Preventing breaches requires stringent adherence to the Uniform Standards of Professional Appraisal Practice (USPAP) and utilizing secure tools and practices. Upholding confidentiality safeguards clients’ interests and maintains the integrity of the real estate industry.

Best Practices for Ensuring Confidentiality

Ensuring confidentiality in real estate appraisals requires adherence to several best practices. Clear and secure communication channels are vital. Appraisers should use encrypted emails and secure file-sharing platforms to transmit sensitive information, minimizing the risk of unauthorized access.

Documentation and data handling are equally important. Appraisers must securely store physical documents and employ secure measures for digital data. For example, using password management tools like LastPass can help in maintaining strong, unique passwords for all accounts.

Professional conduct is also crucial. Continuous education and training on confidentiality standards, such as those outlined by the Uniform Standards of Professional Appraisal Practice (USPAP), ensure appraisers stay informed about the latest privacy protocols. Additionally, appraisers should avoid discussing confidential information in public or unsecured environments.

By implementing these practices, appraisers demonstrate their commitment to protecting client information, fostering trust, and upholding industry standards.

Conclusion

In conclusion, confidentiality in real estate appraisals is paramount for maintaining trust, ethical compliance, and market integrity. Adhering to stringent standards and practices, such as those outlined by the Uniform Standards of Professional Appraisal Practice (USPAP), is essential for protecting sensitive client information. Breaches of confidentiality can lead to severe legal, financial, and reputational consequences, underscoring the importance of secure communication and data handling protocols.

By following best practices—such as using encrypted communication channels provided by major technology providers, implementing secure storage solutions, and engaging in continuous education—appraisers can safeguard client information and maintain the trust and credibility crucial to their profession. Ultimately, upholding confidentiality not only protects clients but also ensures the integrity and fairness of the real estate market, benefiting all parties involved in the transaction. Remember, confidentiality is not just a requirement; it’s a cornerstone of ethical and professional real estate practice.